Understanding Equifax Consumer Credit Report

- 14 May 2017 | 5563 Views | By Mint2Save

When it comes to Credit, your past decides your future, courtesy Credit Reports and Credit Score. Here are some tips which will help you in understanding Equifax Credit Report

The contrasting processes adopted in the banks have often become quite a debate among customers. While banks do not make an intense inquiry about the customer when accepting deposits, the process is really cumbersome when it comes to sanctioning and disbursement of loans.

Apart from the necessary income and profit based interest that banks charge, there is a surplus premium that banks charge, which is obviously due to trust reasons.

The cost of establishing with the customer comes only with the price of interest, which the customer has to bear.

Since the time, lenders have agreed to share to common information about clients who have availed loans, credit score has become the heart of lending. For the banks it is a tool to find out how the financial habits of the customer are. For customer, it serves a method to find out any discrepancy in the loan or someones has used his details to avail a fraudulent loan.

In this article, we will explore details with one such credit score generator, Equifax.

Equifax’s credit reports have been gaining a lot of popularity on a global level recently.

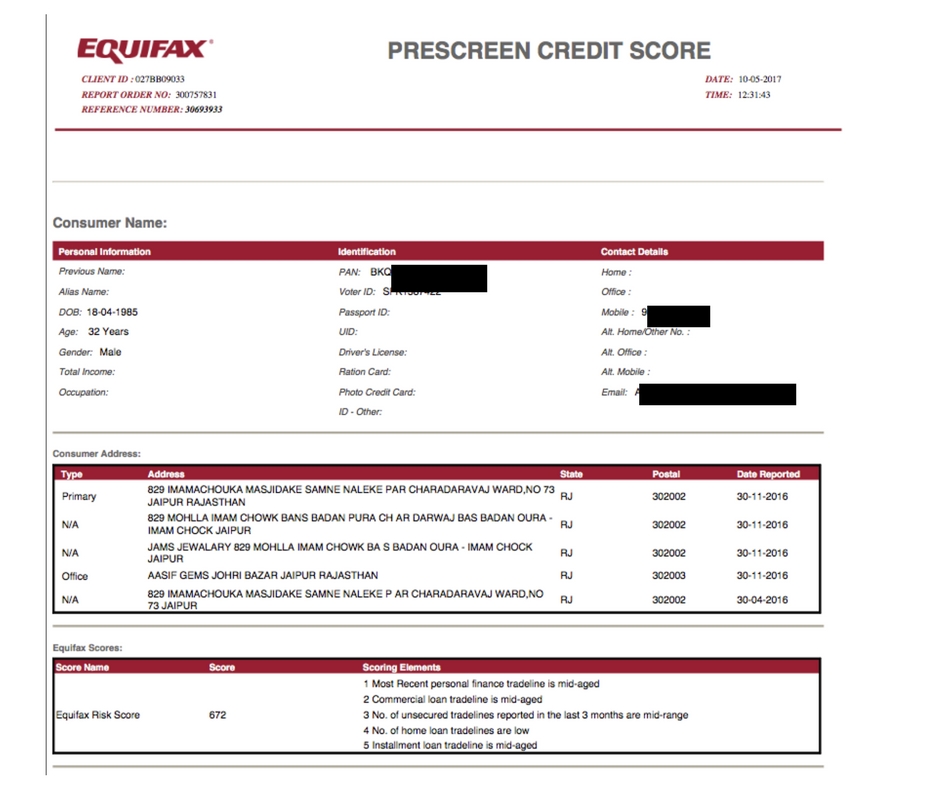

The first page of an Equifax consumer credit report is all about:

- Name and ID Details.

- Address.

- Equifax score along with comments on scoring elements.

It can be divided into three blocks, with each block revealing KYC, communication and credit score summary.

As evident from the image above, the block under “Consumer Name” details not just with the name, but also, date of birth, gender, various identification codes such as driver’s license, UID, PAN card, voter ID etc.

Also, contact details such email, telephone numbers, etc., can be found too.

The last block details with Equifax Risk Score. This risk score is generated on the past interactions in the loan or overdraft accounts. Apart from the score, the scoring elements give a summarized view of how the loan history has been. Scoring elements would reflect upon:

- Brief about recent personal finance trades.

- Type of loan availed, i.e., secured or unsecured.

- Number of loans availed.

- Instalment treatment.

- Any other adverse feature, or loan specific feature.

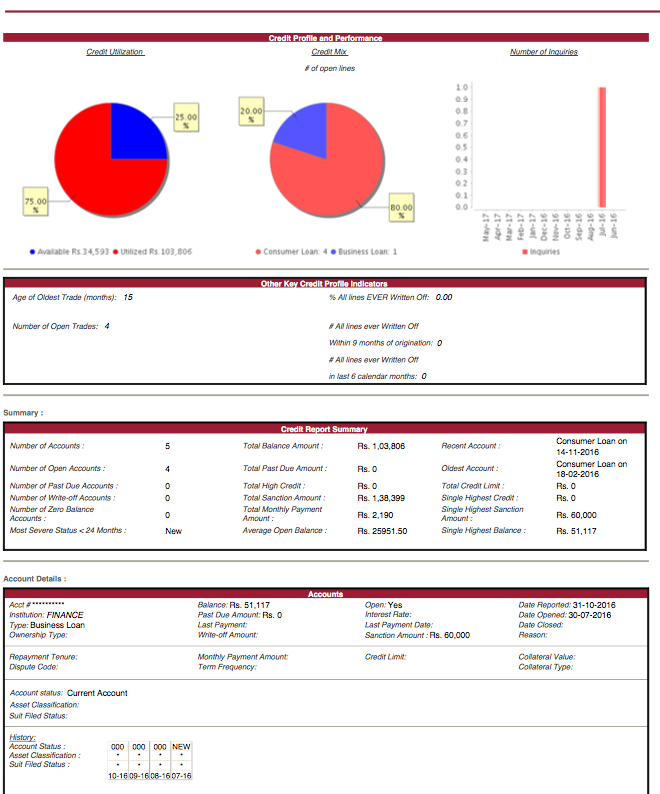

The second page is a continuance of the summary, and describes credit performance and profiles. This feature makes Equifax reports very lucid for a lender, as it includes a pie chart based distribution of debts. Further, a table explaining number of inquiries made on the Equifax is also there.

For any lender, the lesser the number of recent searches on Equifax, the better is the chance of loan proposal being more genuine. Multiple recent searches can simply mean any one or more of the following:

- The applicant has already applied for a loan somewhere.

- The applicant might have availed a loan, which hasn’t been updated on Equifax yet.

- There are multiple lenders searching for the applicant, and have tried to retrieve or update his data via Equifax.

Under the pie chart and table, you can see the credit report summary. This summary details with the total number of times a customer has availed a loan, the total amount outstanding in all loans, average monthly payments, maximum debt the customer has ever witnessed, whether there have been any disputes in any of the previous loans.

Briefing out, page 2 can sum a lot of details about the customer credit related habits. It is a general practice that a customer does not detail with each and every loan that he has availed. Using Equifax, his present as well as past liabilities become crystal clear to the bank.

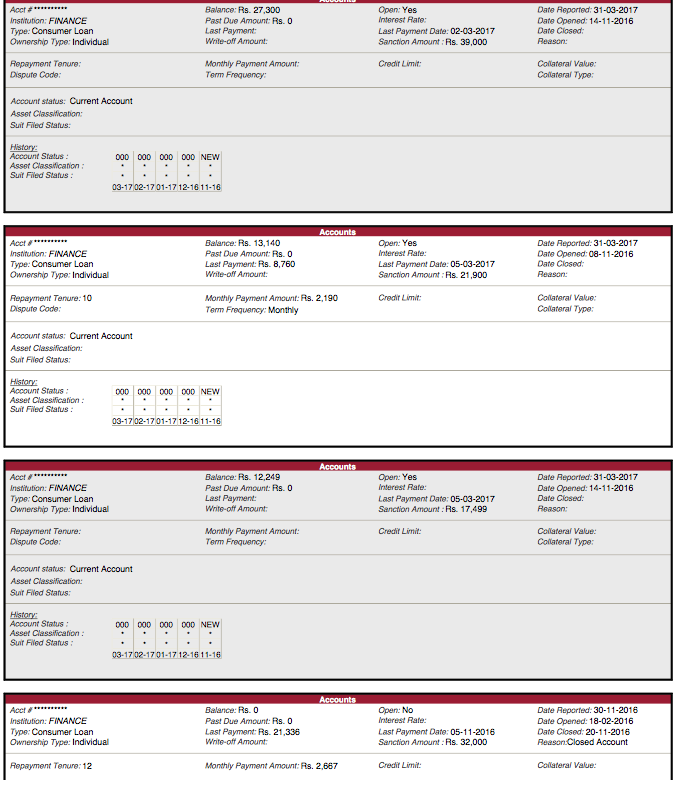

From the third page onwards, you can start viewing upon loan specific summaries. This page about credit would cover all the secured, unsecured loans, irrespective of them being term or overdrafts.

For each loan, you can view the following data:

- Account Number

- The institution from which loan is availed.

- Type of Loan

- Ownership of Loan

- Amount remaining in the loan

- Any dues in the past

- Last actual payment made

- Details about written-off amount (if any).

- Whether the account is still open

- Rate of Interest

- Last date of payment

- Amount sanctioned

- The date it was reported to Equifax

- The date on which account was opened

- The date on which account was closed

Further, one can also the repayment tenure, monthly instalment, dispute code (if any), limit (if a credit card or overdraft has been availed), details about the collateral such as its type and value.

Account status, its classification as per norms are also updated, that either is standard, substandard or a non performing one.

The next table explains about the history of repayment and the dates when the loan was serviced.

Depending upon how many loans the customer has taken in the past, there can be several such records detailing with each and every loan that has been reported to Equifax.

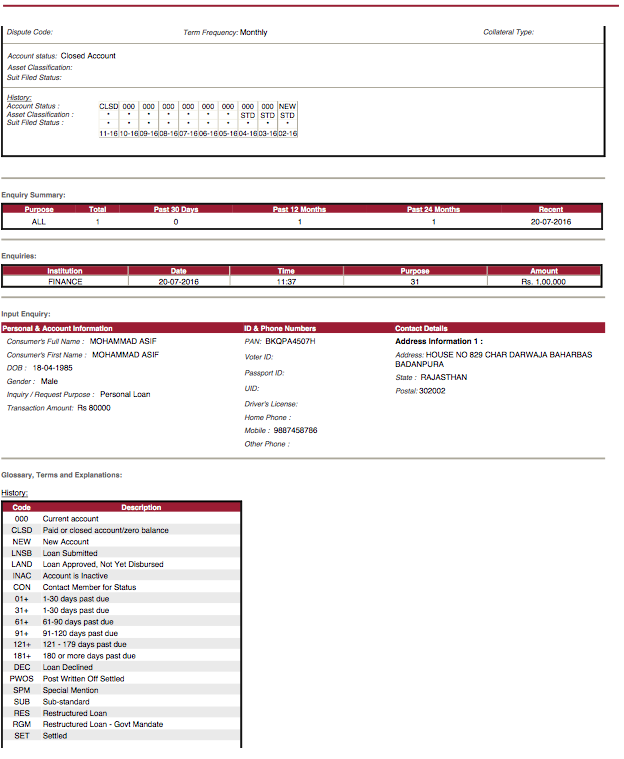

After all the loan details are explored in Equifax, the details that have been input into Equifax for the report can be seen.

These details can be verified from the data that has been shown in the first two pages of the report and it can be checked that whether all details provided are genuine or not.

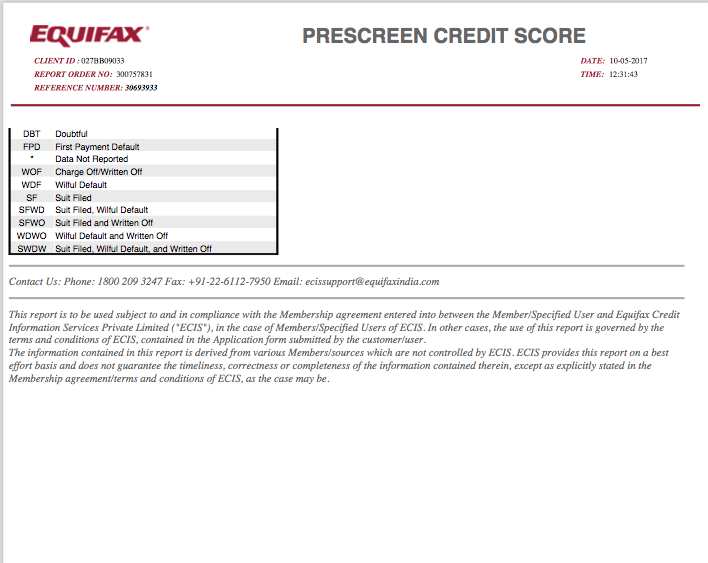

The bottom half part of the previous image and the image above, detail with all the glossary terms that have been used in the Equifax report.

In todays disruptive financial times, credit score generators like Equifax are no less than a boon to the bank as well as the customers.

A detailed credit score can help the bank realize the customer’s basic intention behind the loan, his dedication towards servicing previous loans and decide how risky can the whole transaction be.

A credit report is quite similar to a Blockchain. Data once recorded over it cannot be modified or deleted. Once a loan goes bad, it will always reflect in the credit profile and have an adverse impact on the credit score.

There hasn’t been a solution to device a credit score generation mechanism for those who haven’t availed a loan ever in their lives. As of now, banks rest on the performance of account statements, job profile and standard of living for the same. Let’s hope a custom model is devised for those having nil exposure when it comes to loans.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18107 Views

- 16 June 2020 | 15469 Views

- 19 May 2021 | 15198 Views

- 14 May 2021 | 11892 Views

Recent