Understanding Credit Risk

- 21 May 2017 | 5208 Views | By Mint2Save

The system of organized lending can never run out of risks. Be market, liquidity, credit, interest or operational, risk is inevitable for banks and other financial firms. Hence, a primary importance is given to risk profiling in all financial institutions.

One of the omnipresent risks that have taken a toll on banks regularly is credit risk. In simplest terms, this risk can be defined as non repayment of a loan as per agreed conditions, to the lender, thus ruining the lender’s investment. The non repayment can be intentional (willful default), due to failure of an industry (systemic risk), failure of cross currency settlement (settlement risk) etc.

In this article, we are going to explore credit risk. We will discuss its basic meaning, types, causes, effects and how banks all over the world have made attempts to monitor, mitigate, transfer and at times, accept the risk.

Credit: The Term

As a term, credit holds multiple meanings for various people. In terms of loans, it refers to the whole process of loan processing which includes customer identification and verification, loan appraisal risk rating etc.

What is Credit Risk?

The risk that arises due to inability or deliberate efforts of the borrower to meet lender’s repayment obligations is termed as credit risk. Credit risk does not limit itself to loans and overdrafts only, but is equally applicable to debt based instruments, hedging, trade and several other transaction settlements.

A very common instance where credit risk causes loss is when a bank is unable to fetch instalments or interest from a borrower.

Another example of credit risk is where the bond holder’s coupon payments and principal are not serviced by the bond issuer.

Credit risk has been in the picture since the inception of financial markets and it has formed an essential base of all Basel standards.

Counterparty Risk

Counterparty risk is a type of credit risk when a couterparty fails to meet its repayment obligations, either due to failure or intention. When it comes to finance, counterparty can be called as obligor, as it has an obligation to fulfill the financial commitment.

Issuer Risk

This type of risk can be understood more clearly via an example. Take a company, which has been rated high on credit score, issues a bond which promises regular coupon payments. Now imagine the company taking a severe hit on its business and declaring bankruptcy because of it. It will then stop paying the coupon and might even resist to pay back the principal money of the bond.

This type of credit risk where the issuer defaults on its payment obligations, is termed as issuer risk.

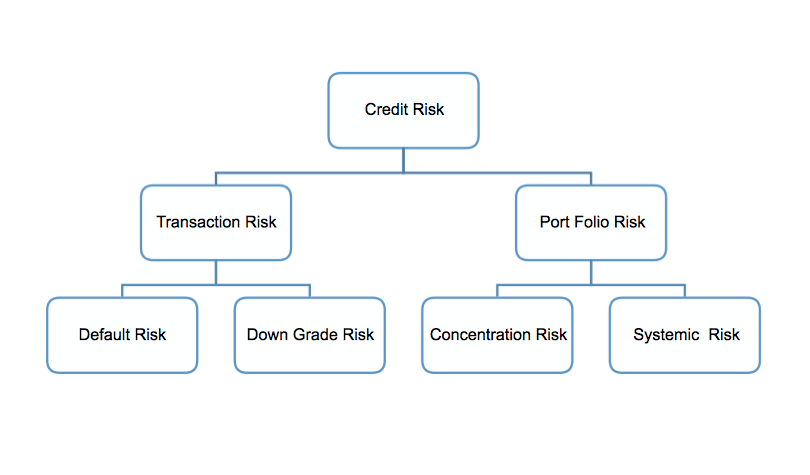

Types of Credit Risks

Proactive risk management techniques have always led to increase in the types of risks, which are dynamically updated in the risk repository. Categorization of credit risk into various categories is no exception to it.

Credit risk can be divided into two parts, which can further be divided into sub types. The following chart eases out the types and sub types for us.

Portfolio Risk

By portfolio, we refer to a lender’s exposure to various investment categories. For any lender, a portfolio can consist of equity, debt and hybrid instruments. Based upon how the portfolio has been created, this risk can be classified into two parts.

Concentration Risk: This risk has evolved from not following the evergreen recommendation of “Putting all your eggs in the same basket“. A party can be called susceptible to concentration risk, when its major revenue/cash flows comes from a handful of large parties. This risk can be defined in various terms, such as:

- Industry/Activity

- Loan size

- Distribution in a region

- Security

- Loan Ratio

- Repayment period

- Interest rate

- Purpose

- Income level

Concentration is not related to the amount invested, rather it is more concerned with the number of baskets (types of investments) that you have. For instance, say you have a 100,000 bucks to invest.

If we follow concentration risk pattern, investing 100,000 between 5 different investments is far riskier than investing the same amount between 10 investments. This means, lesser is the ratio of funds in each investment, less riskier is the portfolio created.

In order to avert concentration risk, central banks recommend prudential exposure limits for every sector and there are credit review committees, which regularly review their exposures to various sectors: retail, corporate, infrastructure, services etc.

Systemic Risk: As the name suggests, systemic risk comes into action when a particular industry fails. For instance, the inconsistence of internet connectivity and power supply in the developing nations can hamper existence of various internet based companies.

The global downturn of the economy in 2008, the burst of the dot com at the beginning of the Milennium, are a few notable examples of systemic risk.

Systemic risks have industry wide impacts and when they strike, it takes a good amount of time for industries to cope up with the trouble. Systemic risk can also trigger other risks such as legal, operational and investment. Some other well known factors that cause systemic risk are:

- Change in interest rates

- Government Policies

- Inflation

- Exchange rate

Transaction Risk

In simplest terms, financial transaction can be termed as the exchange of money for goods or services or exchange of currency. This risk can be divided into two sub categories:

- Default Risk: Default credit risk comes into picture when a borrower fails to meet his payments, as per mutually agreed terms and conditions. This risk does not necessarily exists inside the banks, but can also be dependent on borrowers and external factors.

Internal factors –Applicable to Banks:

- Deficient loan policies

- Inadequately defined powers for sanction of loans

- Absence of prudential credit concentration limits

- Absence of credit committees

- Deficiency in credit appraisal systems

- Excessive dependence on collaterals

- Inadequate/lack of risk pricing

- Absence of loan review mechanism

- Post sanction surveillance

External factors-Applicable to Borrowers:

- Inadequate technical know-how

- Locational disadvantages

- Outdated production process

- High input costs

- Break even point being very high

- Uneconomic size of plant

- Large investment in Fixed assets

- Overestimation of demand

- Wide swings in commodity or equity prices

External Factors-Applicable both to the borrower and Banks:

- Credit worthiness of the counter party

- Interest rate risk

- Forex risk

- Country risk

- Economic scenario

- Government policies

- Trade restrictions.

2. Downgrade Risk: From retail to corporate lending, credit rating has become a mandatory in all sorts of exposures. The probability of a degradation in the credit rating of a borrower during the time when it is under debt, can be termed as downgrade risk. Degrading of credit rating can have high repercussions such as:

a. Necessity to infuse more capital

b. Increase in risk premium.

c. Deterioration in quality of credit exposure.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18237 Views

- 16 June 2020 | 15757 Views

- 19 May 2021 | 15310 Views

- 14 May 2021 | 12033 Views

Recent