The Basics of Mutual Fund – Part 2

- 1 November 2015 | 3610 Views | By Mint2Save

In our previous article regarding basics of mutual funds, their essence for one’s financial security and how well investing in them can reap good returns. Owing to their importance in personal finance, we broke down mutual funds to their basics. In this article, we continue our journey of exploring mutual funds’ basics.

[In case you missed the first one, it is here]

5. Multiple Types of Mutual Fund: Now you might be wondering that when the mutual funds are already color coded, isn’t it obvious that there are mutual fund types. Well, yes and no! Mutual funds cannot be categorised only on the basis of color coded or risk perception.

6. The SIP: Be it any Mutual Fund, this feature is the unique selling proposition, that most of them would try to sell you. SIP or the Systematic Investment Plan is a feature which the elders have used and cherished always from it. Under SIP, you chose a fixed amount of money you want to invest in. It can be low as Rs. 500 or as high as anything. This amount could be invested at regular intervals, mostly, monthly and quarterly. On a fixed date, that fixed amount would be debited from your account and mutual funds units, be whatever the number they are, would be bought. This means that when the fund is priced higher, you buy lesser number of units and when it is relatively more economic, you buy more units.

The units you bought would keep on accumulating and would get priced as per the daily NAV of the mutual fund. What difference it would make is that when the NAV was low, you bought more units, which means that when the NAV shoots up, you are in sheer profit. Good for you! When the NAV goes high, you buy lesser units, which means that if unfortunately the NAV comes down, you are not in heavy loss or losing on your budget. A simple game of demand and price, termed as SIP.

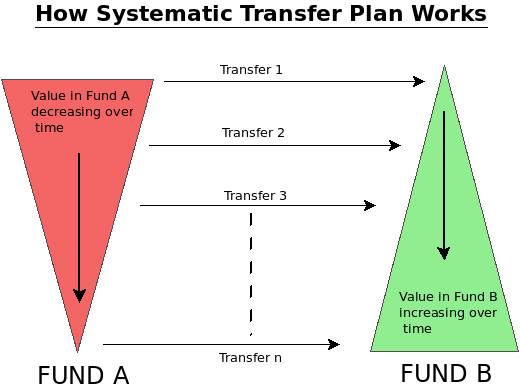

7. STP, SWP: When it can be systematic investment in the mutual fund, why can’t there be systematic withdrawal plans? Well, there are systematic withdrawal plans or SWP, where you can withdraw a pre decided amount of funds from your mutual funds for your use.

Similarly, there are also systematic transfer plans where you can transfer the funds from the mutual fund you are invested into to the other. Interesting, and explore worthy, isn’t it?

8. Tax Saving: Mutual funds have evolved themselves as in interesting tax saving tool too. A few mutual funds, though low on returns, do provide tax saving options. Interestingly, you can adopt a SIP in that too. When you want to save Rs. 24000/year, you can chip in a SIP of Rs. 2000/month into a tax saver. This is one way of saving money, without feeling the burden of parting with a lump sum.

9. Managed by Qualified Fund Managers: When there is money being dealt, it is NEVER that we trust anyone with it. We need proof and we need qualifications. Mutual fund houses, well aware of that part, employ expert market analysers as fund managers. These managers, mix the proportion so well that the fund gets safety from market losses and attains a steady growth when markets is going up. Adding to their qualification and experience, there are software that predict market movements and suggest investment strategies using regression and analytical techniques.

10. Online Investments: Before entering into the securities market, one time KYC is a necessary process. But being just one time, it does enable you to invest in the mutual funds through the internet. Earlier, online mutual fund investment was not preferred much by investors as they do need a convincing statement from the mutual fund distributor. However, now, with the push from mobile applications, online investments are gaining popularity among new age investors.

Some platforms popular over the internet include Kuvera, FundsIndia, Finozen, Scripbox, etc. Some of these platform offer direct mode of investment in mutual funds, other than regular mode. Investing in direct mode saves the investor from certain percentage of commission, which is generally paid to mutual fund advisors.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18237 Views

- 16 June 2020 | 15757 Views

- 19 May 2021 | 15310 Views

- 14 May 2021 | 12033 Views

Recent