How a Credit Card Works?

- 1 May 2017 | 4023 Views | By Mint2Save

A Credit Card is a small debt based financial product that can help you build credit, make suitable payments and meet everyday expenses in people life. Credit cards are financial tools issued by banks and other financial institutions that can save you money, allow you to make purchases, take cash advances, transfer balances from other accounts or completely ruin your finances, based on how you use them.

Earlier, these plastic money instruments were openly criticised for unbearable interest and service fees. Following that, the companies have brought down the service and interest charges, making a credit card accessible to anyone having a consistent source of income. Now, one of the biggest mistakes you can make is to use a credit card without really considering how it works. How a credit card works to get the best of your personal finances is explained below.

How to use a credit card?

When you apply for a credit card then the card provider will ensure that if you are financially eligible to own it or not. If they find you entitled then depending on the amount you earn the Credit Card Company or bank will set a credit limit for you. And then once you get your credit card, you can use it to make payments on credit. If you are using a card it means that you are borrowing money from your card provider (bank). Whenever you swipe the card or do the transaction then you can either use the full or a portion of the credit limit. If you exceed your credit limit, you will have to pay a penalty for it. Don’t be lure to use credit cards at cash machines to take out money otherwise you might get hit with charges up to 4% or more with some companies.

Finally after every billing transaction, the lender anticipates you to repay the amount you have borrowed from them as it carry fixed interest period, within which the cardholder is made-up to pay either the full amount due by him or a part of it. The cardholders do not have to pay any interest on their card if they pay the full due amount otherwise they will have to pay an interest on the outstanding balance and on the new purchases if they pay only the minimum amount due or do not repay any money. The card provider will keep charging the interest until they pay the full outstanding balance. If cardholder don’t pay off any outstanding balance in full then interest will be charged. Thus, it is normally advisable to pay off the bill every month.

Process of credit card:

When a credit card holder swipes his/her credit card to make payment at a seller or merchant outlet then a request is submitted by the merchant to the acquirer either through phone or network connection.

The acquirer passes this request to the issuer of the card to allow the transaction. To make a purchase the card issuer has to check if the cardholder has sufficient credit available in his/her account.

If enough credit is there, then an authorisation code is sent to the acquirer by the issuer, who then approve the transaction and the purchase is made.

A merchant does not swipe just one card on the Point of sale machine in one day. Based on the number of customers, there can be many requests sent to the acquirer by the merchant.

Suitability of credit card

Unless you are in introductory period, a credit card is typically just right for you if you are sure that you will give back the amount you borrow every month.

For full monthly outstanding balance, or at least the minimum amount to be paid from your bank account then set up a direct debit. This will help you out to avoid unnecessary charges and the loss of any introductory incentives.

You will undergo a credit assessment when you apply. A good credit rating will improve your chances of a successful credit application. It could also give you right to use cards offering the lowest interest rates or promotional offers.

You must be at least 18years to apply for a credit card. With some cards, the minimum age is 21.

Advantages of having a credit card

1) It is easy to carry: Credit cards are very convenient and accepted at more places than charge cards and prepaid cards.

2) Safer: If your card is lost then just call your bank immediately and cancel it. If it is stolen and used illegally then you are much more likely to get the money back.

3) Easy to use: With the help of credit cards you are protected for any purchase over $100 and below $30,000. So, if you purchase a defective TV and the seller won’t refund your money then the credit card company will repay you.

4) Pay late and by now: If you do not have the cash and you need to pay next day then a credit card provides you a few extra financial wriggle room but you must only use it if you’re confident you can pay it off.

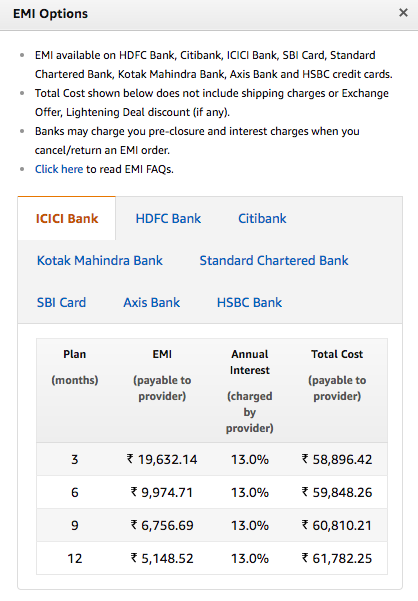

5) Offers: Some credit cards might often get things like air miles, reward points or cash back. For instance, you can check the one below where products can be purchased on an EMI via your credit card.  EMI On Credit Cards

EMI On Credit Cards

Disadvantages of having a credit card

1) Extra fees: While having a credit card you could find yourself paying additional fees or penalties because for exceeding your credit limit or missing a credit card payment on time. There are usually additional fees, for example using a cash machine.

2) Interest payments. While having a credit card then you must clear your balance at the end of each month otherwise you will have to pay interest on that outstanding balance.

3) Costly to use abroad: It depends on the card as some are designed for travellers and others might find are very expensive when it comes to fees and other charges.

So, money is just a poor man’s credit card.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18237 Views

- 16 June 2020 | 15757 Views

- 19 May 2021 | 15310 Views

- 14 May 2021 | 12033 Views

Recent