Everything About National Pension System

- 23 April 2017 | 4909 Views | By Mint2Save

National Pension System or NPS is a voluntary, defined contribution retirement savings scheme or the pension scheme launched by the Government of India with the objectives to provide the old age retirement income to all the citizens, extending old age security coverage to all citizens and reasonable market based returns over the long run. The NPS’ main aim is to set up pension reforms and to encourage the habit of saving for retirement amongst the citizens. NPS is considered one of the best best tax saving instrument. It is regulated and managed by PFRDA (Pension Fund Regulatory and Development Authority), which is also an undertaking of the Government of India.

Under National Pension scheme, an investor can open the two accounts i.e. Tier I and Tier II account. Tier I account is a non-withdrawable and permanent retirement account while Tier II is a voluntary withdrawable account. Download the NPS Form here: NPS Form.

NPS is relevant to all new employees of Central Government service and Central Autonomous Bodies except the armed forces and it is also applicable to all the employees of State Governments, State Autonomous Bodies, with effect from 1st January 2004 and all citizens falling between the ages brackets of 18 to 60 years have the eligibility for investing in the National Pension System and few of the applicants that cannot join NPS are undischarged insolvent, Individuals of unsound mind and Pre-existing account holders under NPS.

Benefits associated with the National Pension System is that It is transparent and cost effective system in which the pension contributions are invested in the pension fund schemes and this will help an employee to know the value of the investment on day to day basis. It is very simple to use as all the subscriber has to open an account with his/her nodal office and get a Permanent Retirement Account Number i.e. PRAN. Through NPS each employee is identified by a unique number and has a separate Permanent Retirement Account Number which will remain same even if an employee is transferred to another office. It also offers the choice of Funds, Service providers, Investment Options, Annuity Service Provides, Pension fund Managers and Annuity Plans to all Subscribers. The National Pension System is regulated by the Pension Fund Regulatory and Development Authority i.e. PFRDA.

It also provides all the Subscribers the freedom to switch between different Pension Funds . It carries extremely very low cost of operations.

The subscribers also get tax benefits on the contribution made in this scheme under section 80C of the Indian Income Tax Act.

The important documents need to be submitted to the POP for the opening of a NPS account is, filled in subscriber registration form (NPS application form),Affix a color photograph on the application form, Proof of Identity, Proof of Address (ADHAR Card/ Bank Statement/ Voters ID/ Passport etc..). With all the details send, do not EVER forget to mention your email ID as it becomes very convenient once you register your email with NPS. All the transactions etc., can be monitored regularly via the statements NPS sends to you.

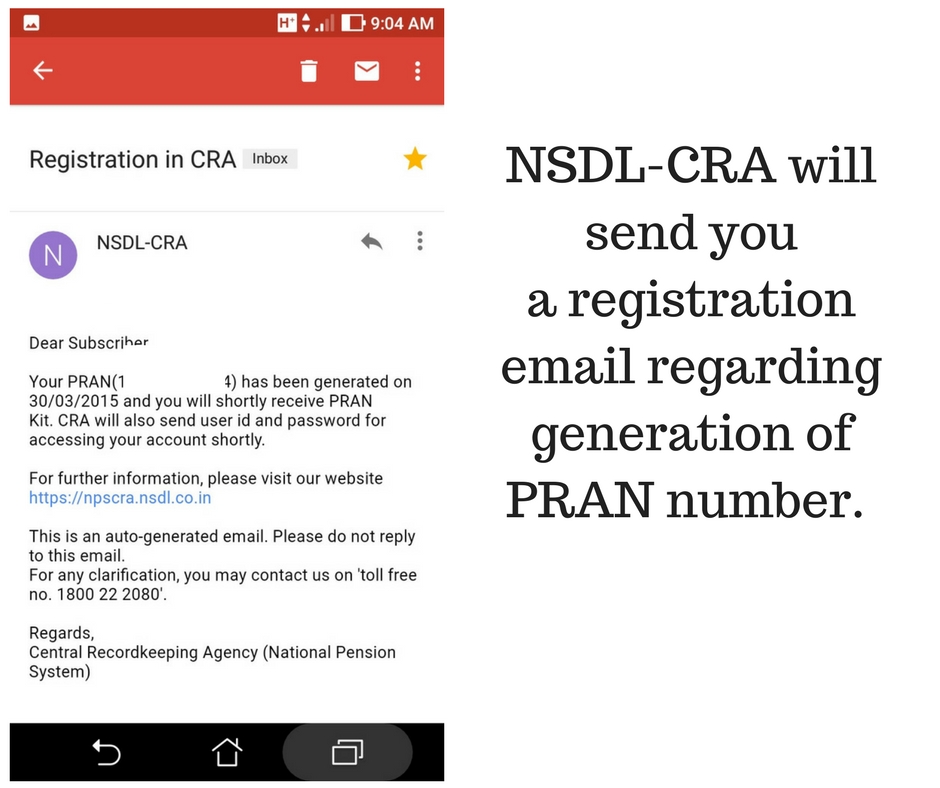

Upon submission of the documents along with the form, you will have to wait for a period of approximately 15 days till your NPS account becomes fully active. You will get an email like the one mentioned below. This email is an intimation about generation of your PRAN number.

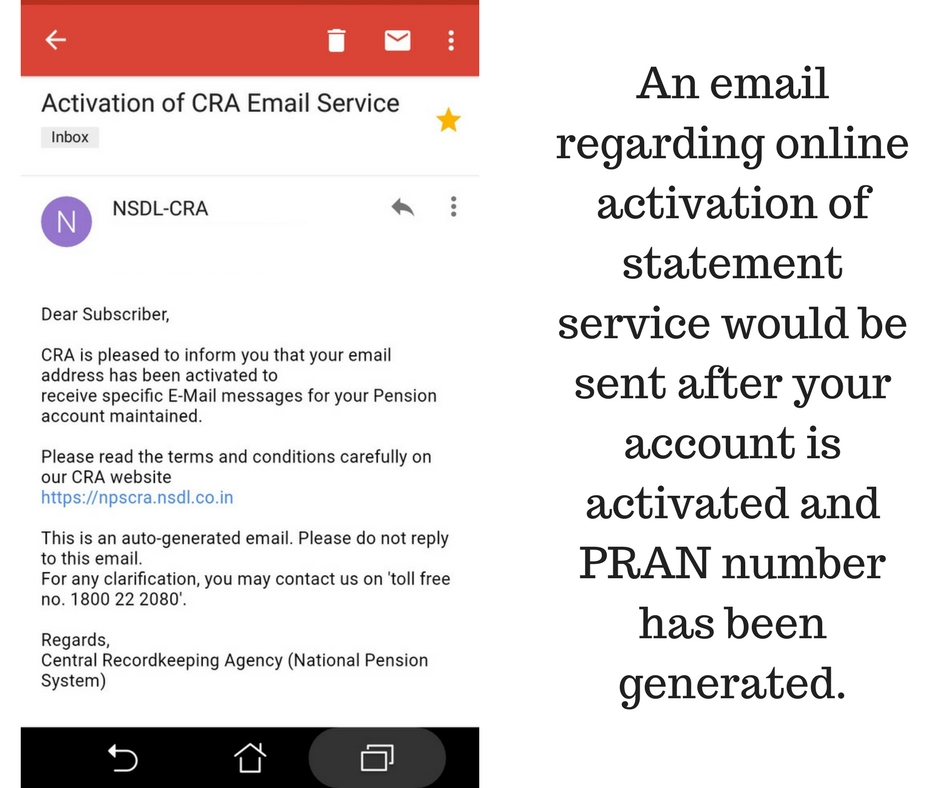

In the previous paragraphs, we have informed you to update your email address in the form for NPS. CRA, i.e., the Central Record Keeping Agency, further sends this email:

Even though there are various reasons or misconceptions about NPS for the millions of potential investors as a NPS scheme for individuals does not provide tax benefits of more than the Rs. 1 lakh limit available for investments. It is also one of the few government schemes that provide investors with the options of the funds in which they intend to invest.

NPS allows only phased withdrawal (not any longer) and you cannot take the money after retirement when you need it. The Government will not be making any contribution to your NPS account. NPS invests in equity too, that means it could be very risky. NPS is like other pension products like EET (exempt exempt taxed) that means it will be taxed afterwards, when you ultimately receive the money. As the private fund managers manage the money so there is a risk that they may cheat you in terms of cost. Another disadvantage is it involves competition of traditional schemes.

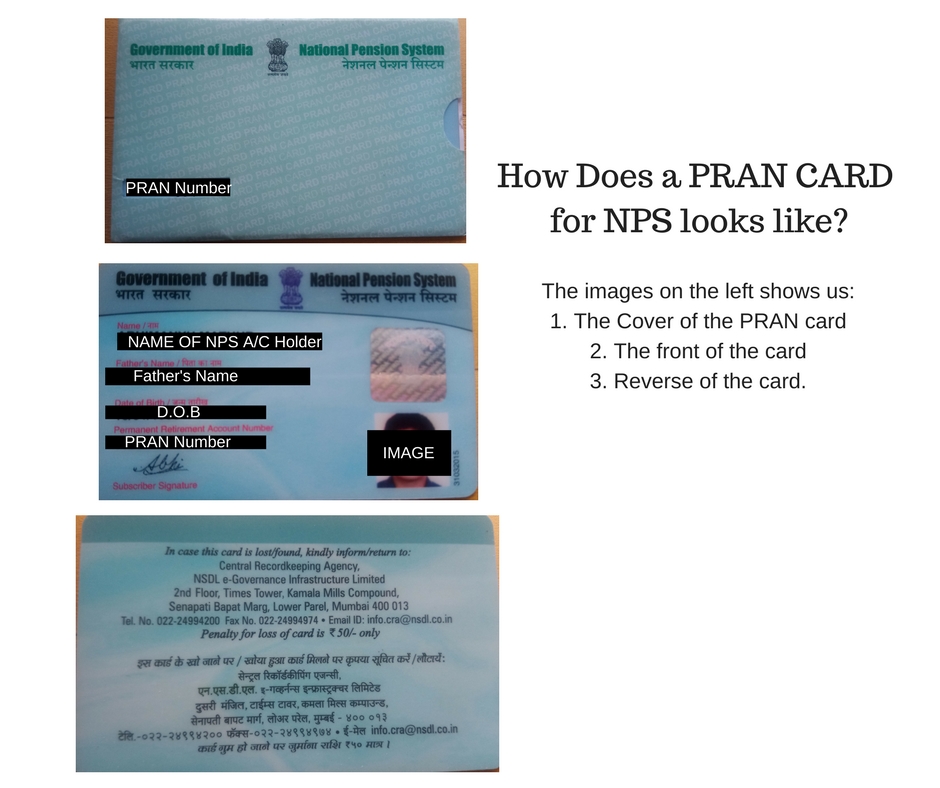

NPS CARD with PRAN Number

For every NPS subscriber, a card is issued which looks like this:

NPS Statement

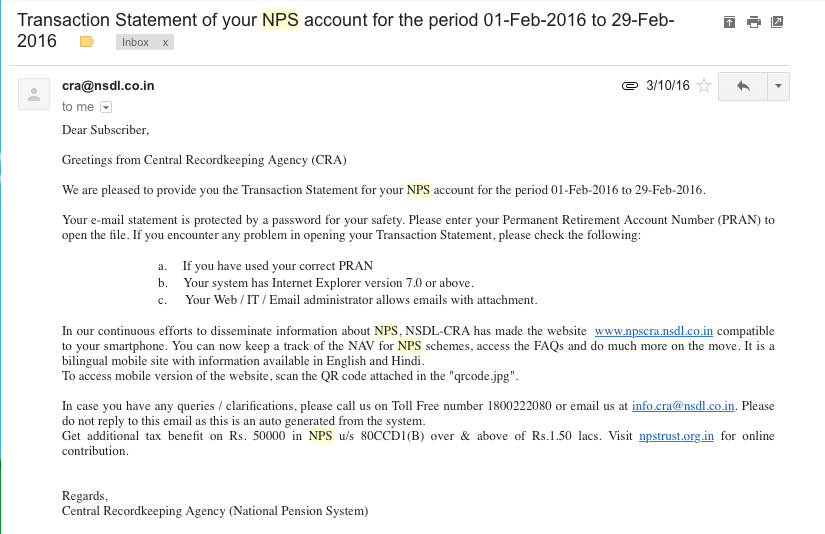

Every month, after PFRDA receives the contributory credit in your NPS account, you get an email regarding the same. Along with the email, a statement is attached for your personal accounting purposes.

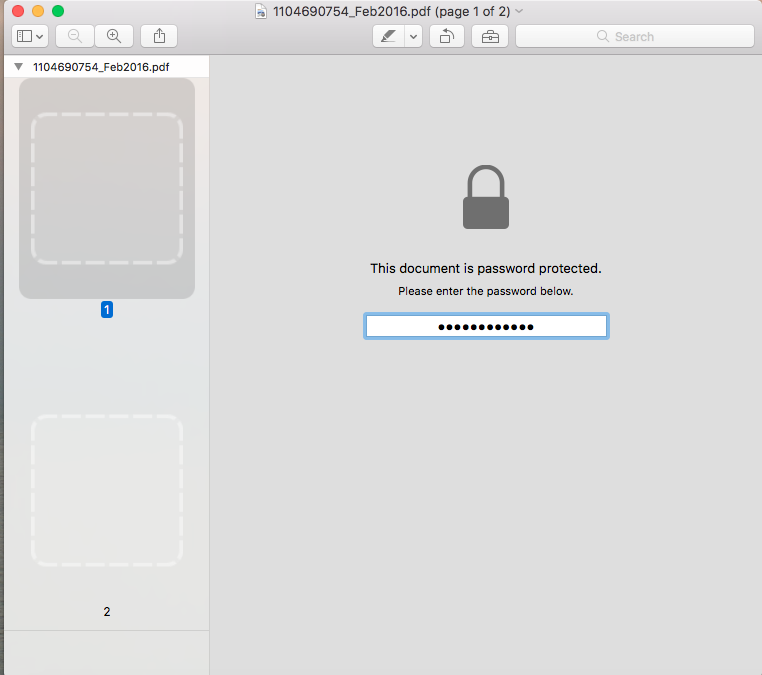

This email is password protected and the password is your PRAN number:

As you can see the password protected interface of the NPS statement does not display any sort of information.

As you can see the password protected interface of the NPS statement does not display any sort of information.

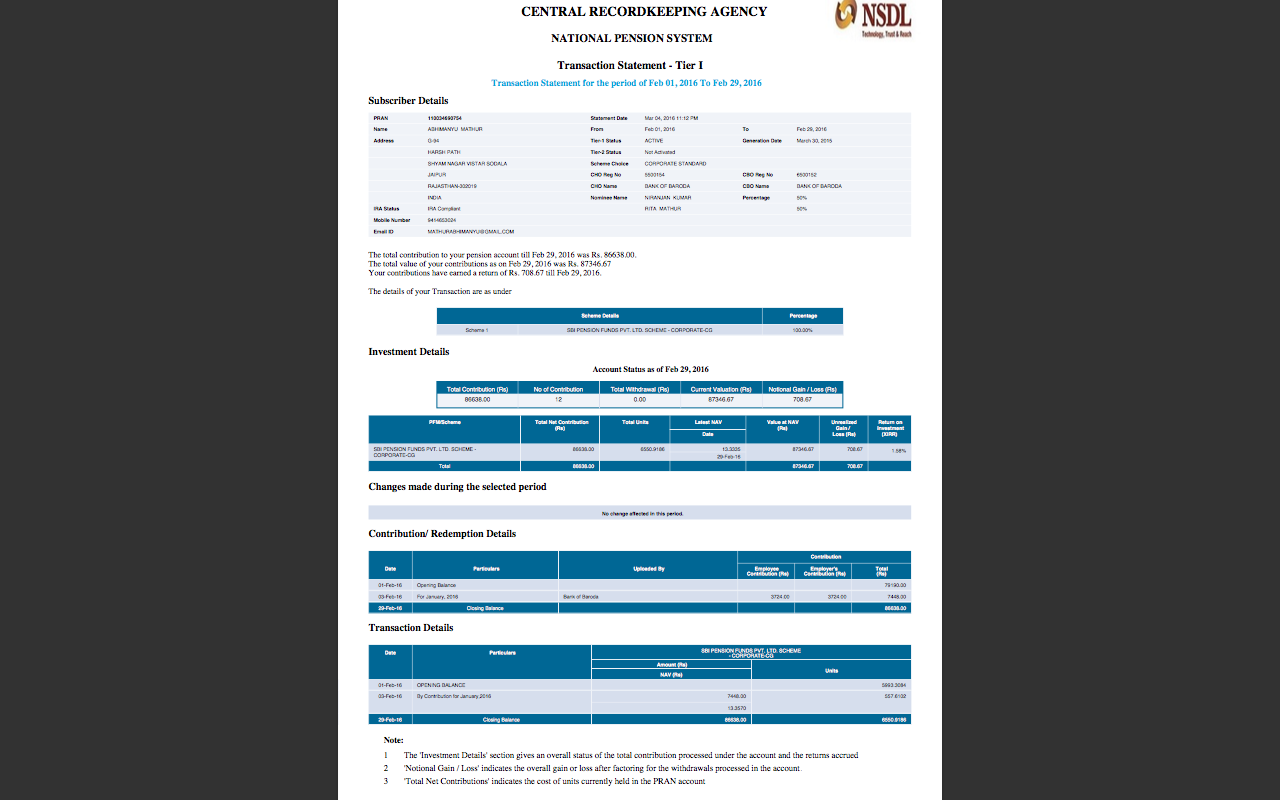

Once the password, i.e., the PRAN number is inserted, you will see a two page statement would appear. It would detail with the following:

- Name and other relevant details of NPS subscriber.

- Fund Chosen by the subscriber.

- Value of the fund and returns.

- Other important terms and conditions of the transaction.

As anyone can observe, appearance wise, this card is quite similar to a PAN Card. However, the end uses of these two are totally different. This card comes in handy when you switch over organisations, but want to keep using the same system of NPS for retirement plans.

A minimum annual contribution has to be made by the subscriber of Rs.6000/ for his Tier I account in a financial year and if not contributed to the account will be frozen.

To unfreeze the account, the customer has to pay the minimum contributions for the period of freeze on the account, the minimum contribution for the year in which the account is reactivated and a penalty of Rs.100/-. There are no entry and exit loads. Withdrawal facility is there as when you wish in tier II.

As far it is concerned with the structure and cost, NPS is the best retirement option. Thus, the National Pension System is an attempt towards finding a practical retirement solution by encouraging the habit of savings amongst the citizens and offer retirement income to each and every citizen in India.

The greater the investments achieved if greater would be the value of the contributions, the longer the term over which the fund accumulates and the lower the charges deducted, the larger would be the eventual benefit of the accumulated pension wealth likely to be.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18237 Views

- 16 June 2020 | 15756 Views

- 19 May 2021 | 15310 Views

- 14 May 2021 | 12031 Views

Recent