CIBIL : A complete Crash Course to Consumer CIBIL Report

- 16 October 2015 | 9149 Views | By Mint2Save

Have you ever wondered that what is CIBIL Score or Report?

When it comes to the masters, it is rare that they are at fault. We keep the same thing at mind, when we are seeking immediate or non-immediate financial assistance from recognized organizations like banks. Most of them, including government owned banks, are computerized and tend to defy the theory of being safe and take their time in testing customer’s patience, when it comes to giving loans.

Out of several computerized tools that the banks use to analyze how good borrower are you, one vital and probably the easiest, is CIBIL.

Expanding itself into Credit Information Bureau of India Limited, CIBIL is a masterpiece crafted by HDFC Bank, SBI and Dun and Bradstreet. An automated credit report analyzer, CIBIL fetches everything that you have ever borrowed from any bank or non-banking financial entity. It not only takes into notice of how much and how many loans you borrowed but also keeps a track of how well you actually are in paying it back.

Based on these two criteria, it gives a rating to you. Yes, just like you get marks in an examination, CIBIL also tends to grade/mark you. The higher you get, the better borrower you are.

So, how does it collect the data for all the rating it does?

Let’s take it to the basics to understand the idea. When it came to excelling in the examinations at school or college or any competition, you are expected to attend multiple subjects. Examination for every section gets separately evaluated. What you get as a result is the cumulative marks out of the maximum and along with comes a grade which actually is an average of all the exams you gave.

Now replace the exams with the banks you dealt with and the marks to the repaying tendency you adopted. The better you performed every time, the better was your grade. However, if you failed in one, your performance gets tripped right away. Replace “failed” here with you not being able to repay back the advance.

What the mix gets you here is your CIBIL score. You do well; you are promoted and might get those phone calls and messages where several banks are dying to give you their loans and credit cards at cheap rate of interests. You do bad, you will face a tough time getting more. In standard terms, the score you get is your credit score and the report is called Credit Report.

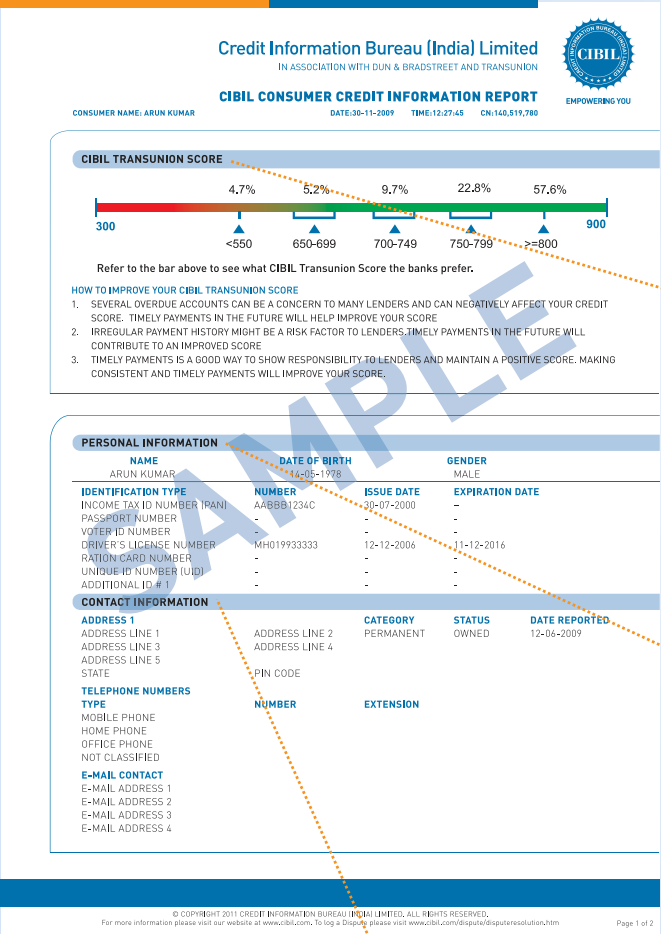

Wonder how a normal CIBIL report looks like? Check it here.

After reading this, common query for those going to the bank for the first time to take a loan is that: What if I never took a loan before? It is simple, the report comes up saying that there is no credit history to show you loan status.

Another query can come up here is that: Why would any bank disclose its advances to agencies where it does not have a share? This works on a simple policy of give and take. You detail with the advance and the nature of the repayment and what you get is an honest and unbiased response making you decide whether you should give the money (which is not yours) or not.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18230 Views

- 16 June 2020 | 15751 Views

- 19 May 2021 | 15304 Views

- 14 May 2021 | 12024 Views

Recent