7 Myths About Life Insurance

- 26 May 2016 | 4905 Views | By Mint2Save

It is uncanny that how often India had been depicted as an economy facing perennial drought when it comes to life insurance. After the advent of Prime Minister’s Jeevan Jyoti Yojna, there was marginal improvement in the percentage of insured, but out of those availing this facility, mostly were those people who already had an insurance. Obviously, something does prevent our over enthusiastic investors in creating a protection cover for themselves. Being mis marketed, is one prime reason. A lot of myths and facts have surfaced up around Life Insurance, that when pondered upon, not only reduce the worth of the product, but also make the person confused about the ultimate aim of the product. In this article, we discuss some most popular myths that revolve around Life Insurance policy.

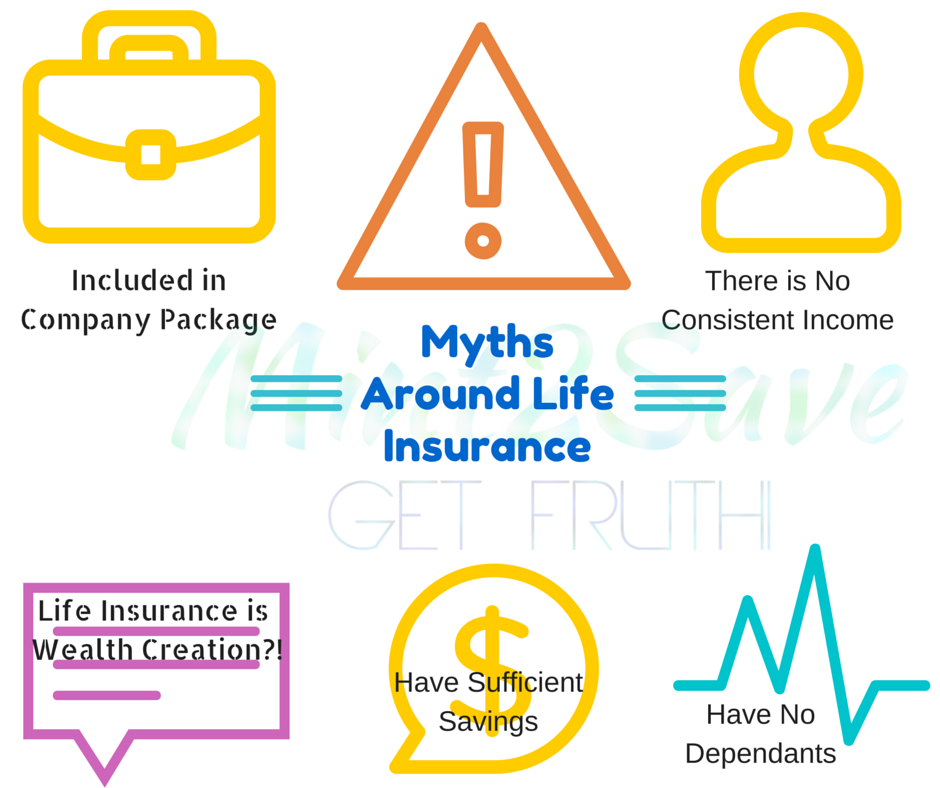

1. A tax saving instrument:

Ultimate aim of making life insurance tax free was to promote it to the masses and make them get double benefit. However, sadly, life insurance is being aggressively sold as a tax saver by almost all insurers. Diverting from the idea that life insurance hasn’t been made for tax saving purposes, it does hamper one’s tax saving planning. There are a lot more and significantly better tax saving options available for tax saving other than a life insurance policy.

2. Wealth creator:

Creating Wealth through a life insurance policy is also one of a kind mis-marketing ideas where the potential insured (misinterpreted as an investor) is promised of wealth creation. A normal practice, that encourages someone to take a life insurance policy so that he can retire richer, or get sudden inflow of money after a certain time, is simply waste of the term “insurance”. These products, when analysed properly,

3. Only for those who have dependants:

“Insurance provides a financial cushion to your loved ones when you are not in this world”, this popular marketing tagline takes loved ones as to be dependants. However, it is also a useful product when you have no dependants, i.e. everyone in your family is earning well. In this case, life insurance would be useful to settle any debts or borrowings. Moreover, with the riders of critical illness etc., the burden of your care would be handled by the insurer itself, thus no one comes under pressure when the expenses are to be taken care.

4. Complicated Claim Process:

The claim process USED to be a cumbersome task, as it had a lot of formalities to be taken care of and the beneficiaries found it hard to redeem the policy without any help of someone who knew process and the people involved in the claim redemption process.

Providing a sound customer support has become a prime task for life insurance companies and they do have a dedicated claim redemption department.

5. Presence of Consistent Income:

Often life insurance is termed as a financial product only for those having regular and consistent income. Not true!! Insurance is needed to cover even one’s kids (investment for a safe future) or spouse is not working but does take care of the house.

6. Added in the Company’s Package:

Often the youth would be heard quoting that they don’t need to buy an insurance policy as their company already has them protected. This is an added perk, and being standard in most companies, these insurance policies do not cover adequately. Also, the policy gets forfeited once the employee leaves the company. It is thus recommended that apart from insurance that your employer provides, get another one, which has a larger sum assured.

7. Have enough savings:

Your savings would never be enough to compensate for your life. The amount in the life insurance is huge and can handle the immediate and deferred needs easily for you. Having high amount in savings are undoubtedly a wise financial planning decision, but replacing that with life insurance is not what we recommend.

Related Posts

Subscribe to get the best of finance and fintech. Regularly.

Categories

Popular

- 31 May 2016 | 18242 Views

- 16 June 2020 | 15763 Views

- 19 May 2021 | 15315 Views

- 14 May 2021 | 12036 Views

Recent